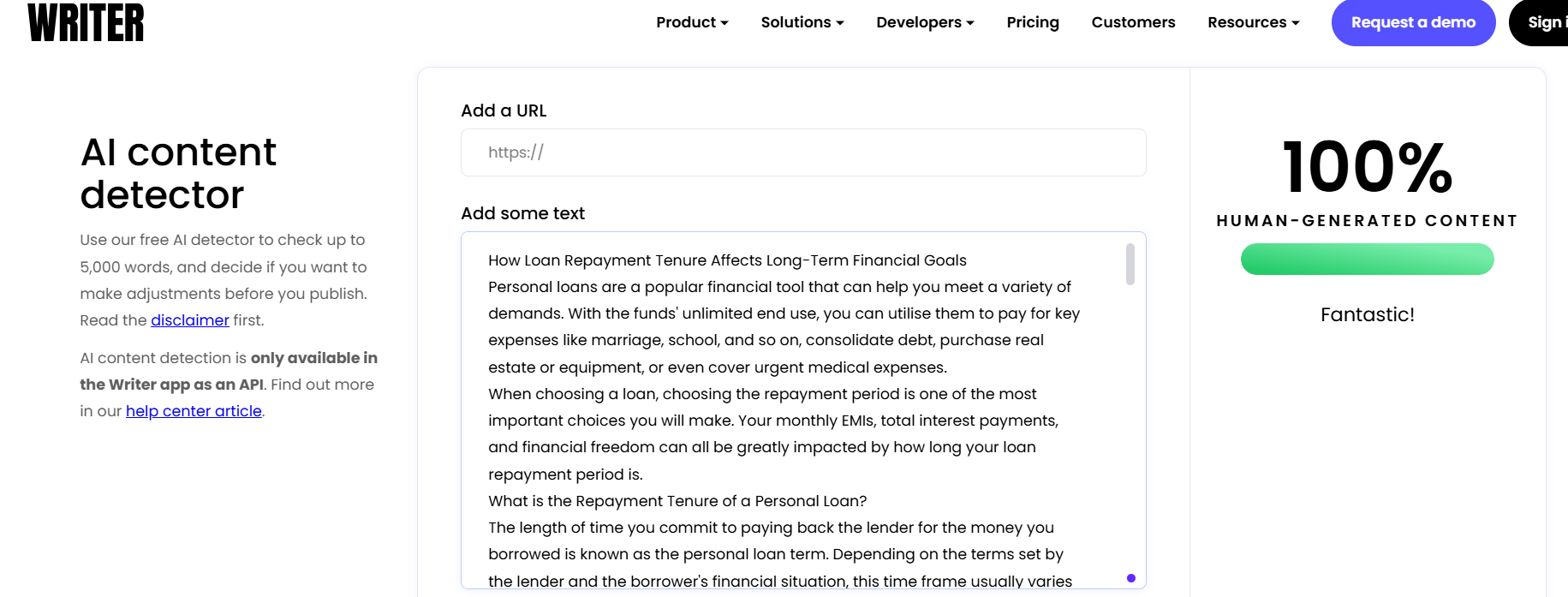

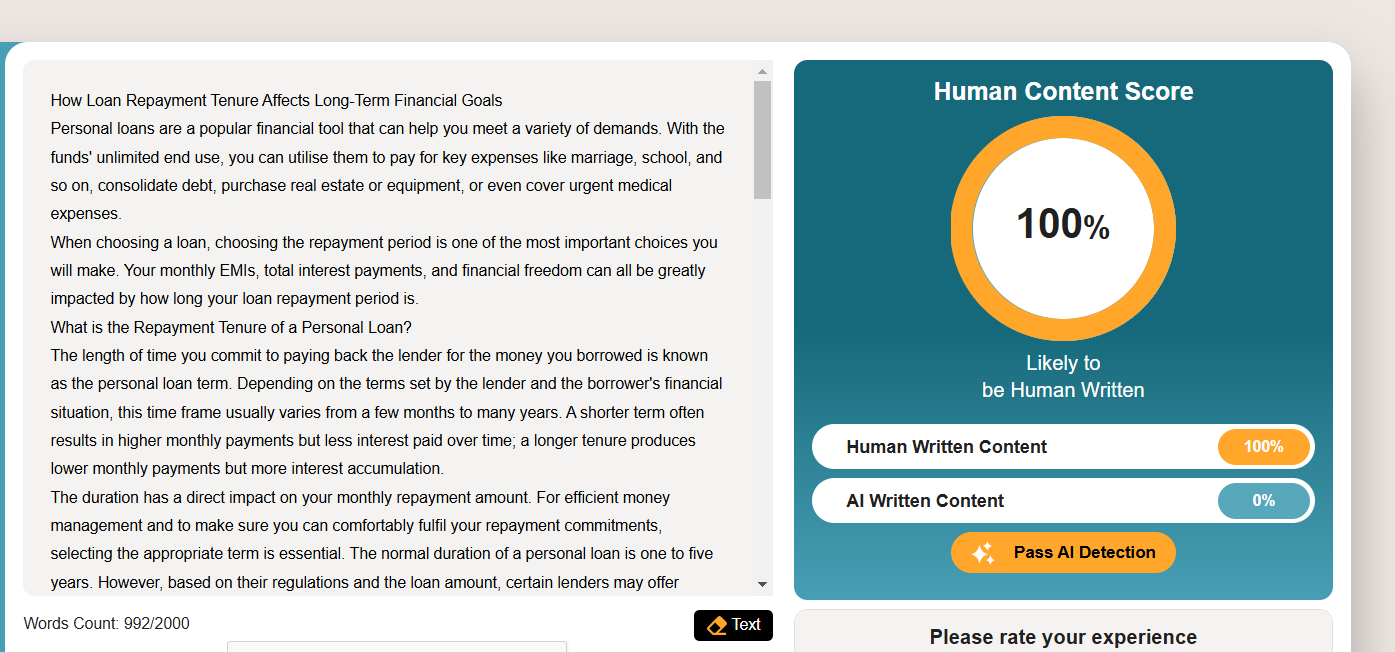

How Loan Repayment Tenure Affects Long-Term Financial Goals

Experience the all-new Kotak Netbanking

Simpler, smarter & more intuitive than ever before

Popular Products

Show More

Quick Help

Show More

Frequently Asked Questions

Show More

For Kotak Bank Customers

For Kotak811 Customers

Experience the all-new Kotak Netbanking Lite

Simpler, smarter & more intuitive than ever before. Now accessible on your mobile phone!

Because Banks take into account your current EMIs when assessing your Personal Loan eligibility. A longer tenure may result in higher EMIs over time, which could reduce your borrowing capacity for other loans, as lenders will factor in your existing financial obligations.

Prepayment of your home loan might give you a lot of flexibility by lowering your EMI or reducing the length of your loan. While it does not directly impact the EMI amount, it can decrease overall loan tenure. Thereby, it potentially results in a lower total interest payout.

Although they have higher monthly payments, shorter loan tenures typically save you more money altogether. Thus, shorter-term, low-interest Personal Loans are best to save you money.

Disclaimer: This Article is for information purposes only. The views expressed in this Article do not necessarily constitute the views of Kotak Mahindra Bank Ltd. (“Bank”) or its employees. The Bank makes no warranty of any kind with respect to the completeness or accuracy of the material and articles contained in this Article. The information contained in this Article is sourced from empaneled external experts for the benefit of the customers and it does not constitute legal advice from the Bank. The Bank, its directors, employees and the contributors shall not be responsible or liable for any damage or loss resulting from or arising due to reliance on or use of any information contained herein. Tax laws are subject to amendment from time to time. The above information is for general understanding and reference. This is not legal advice or tax advice, and users are advised to consult their tax advisors before making any decision or taking any action.

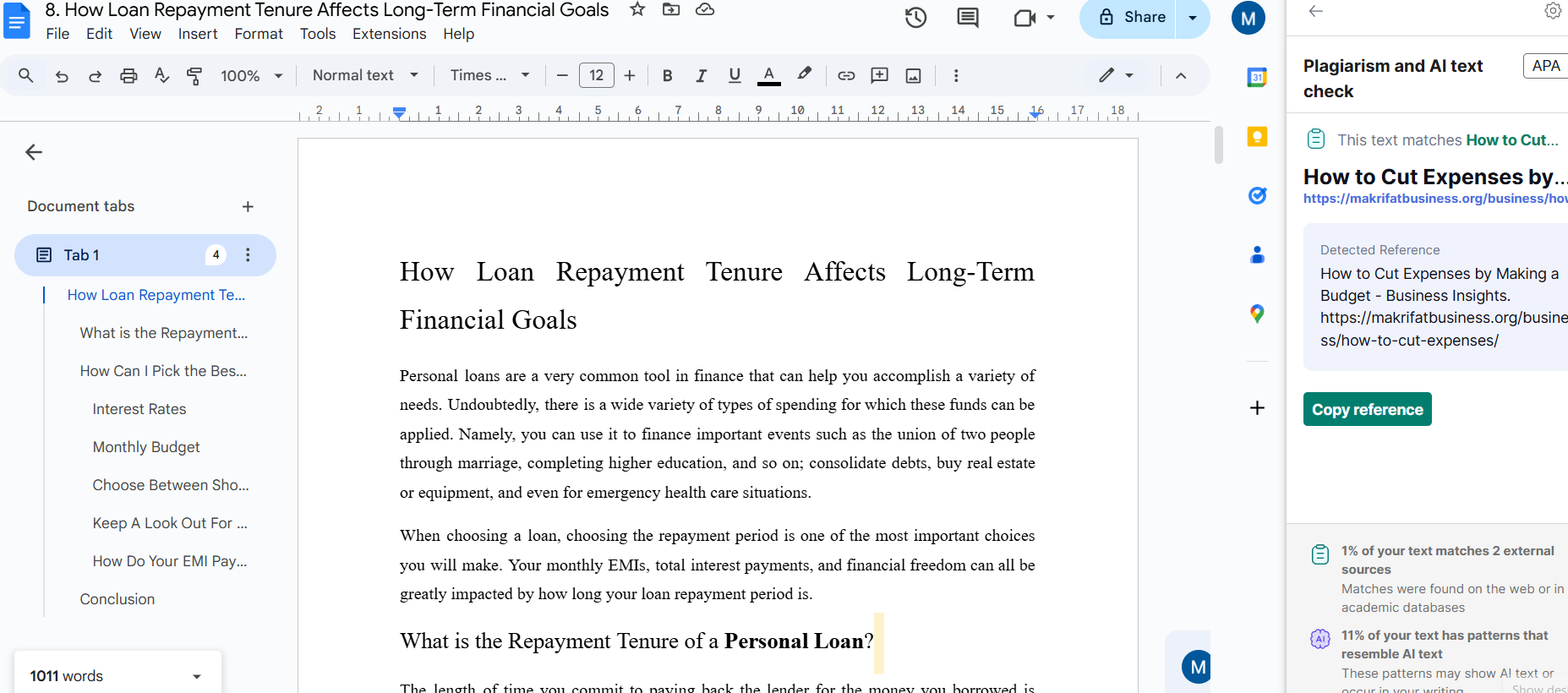

Personal loans are a very common tool that can help you accomplish a variety of needs. Undoubtedly, there is a wide variety of types of spending for which these funds can be applied. Namely, you can use it to finance important events such as marriage, completing higher education, consolidating debts, buying real estate, and even for emergency health care situations.

When choosing a loan, choosing the repayment period is one of the most important choices you will make. Your monthly EMIs, total interest payments, and financial freedom can all be greatly impacted by how long your loan repayment period is. Read on to learn about all the important details here!

What is the Repayment Tenure of a Personal Loan?

The length of time you commit to paying back the lender the money you borrowed is known as the Personal Loan tenure. Depending on the terms set by the lender and the borrower's financial situation, this time frame usually varies from a few months to many years. A shorter term often results in higher monthly payments but less interest paid over time; a longer tenure produces lower monthly payments but more interest accumulation over the years.

The duration has a direct impact on your monthly repayment amount. For efficient money management and to make sure you can comfortably fulfil your repayment commitments, selecting the appropriate term is essential. The normal duration of a Personal Loan is one to five years. However, based on the regulations and the loan amount, certain lenders may offer lengthier tenures.

How To Pick the Best Personal Loan Repayment Term?

Picking the loan repayment term can be a hassle, but here are a few things to look out for:

Interest Rates

The Personal Loan interest rates influence the overall cost of borrowing. A higher interest rate may directly impact your choice regarding the loan tenure since it may result in higher interest throughout the loan tenure. When interest rates are high, the monthly EMI (Equated Monthly Instalment) will be higher, so you might prefer to extend the repayment period to make the payments more manageable. On the other hand, when the interest rate is low, the EMI will be smaller, allowing you to repay the loan more quickly, based on your salary and budget.

Monthly Budget

One of the most important things that helps you choose the right tenure is your budget. To determine the residual income, make a note of your monthly obligations and compare them to your monthly income. You can choose a repayment term that fits well inside your budget and doesn't put you under extra financial strain each month based on what's left over.

To find out how much you can easily put toward loan repayments, you must evaluate your monthly income and expenses. Lower EMIs from a longer term might be easier to manage within your budget. Use a Personal Loan EMI calculator to get a fair idea.

Choose Between Short-Term vs. Long-Term Repayment

Your financial goals and preferences should guide the repayment period you select. Generally speaking, short-term repayments result in lower total interest payments but larger monthly instalments. On the other hand, choosing a longer term can ease the monthly payment strain and provide more flexibility to your budget.

At Kotak Mahindra Bank, you get repayment terms of up to 6 years. Choose a repayment period based on your plans, budget and comfort level after taking your financial goals into account.

Keep A Lookout For Financial Goals

When deciding on the repayment period, take your short- and long-term financial goals into account. Choose a tenure that allows flexibility if you have other financial obligations or expect your income to fluctuate. To provide you with more financial flexibility, some lenders let you change the duration or make prepayments during the loan period.

If you have a salary and are scheduled for a raise soon, you will have more money available to pay a higher monthly instalment. By doing this, you lower the total amount of interest paid on the loan in addition to paying it off early. This examination will be very beneficial in the near future, but it may impose an additional strain till the hike.

Summing up

Choosing the ideal Personal Loan term requires striking a careful balance between controlling your monthly cash flow and lowering your overall interest expenses. Making a wise financial decision requires striking a balance between the requirement for affordable monthly payments and the goal of reducing total interest payments. To find out how alternative loan tenures impact your EMI for a specific loan amount, use a Personal Loan EMI calculator. The EMI for several loan terms will be displayed to you. You can make sure that your Personal Loan experience smoothly fits with your financial goals by making an informed choice. Choose the best repayment plan for you—Apply for a Kotak Personal Loan today!

You have already rated this article

OK