How to Choose Between Fixed and Floating Interest Rates for Personal Loans

Experience the all-new Kotak Netbanking

Simpler, smarter & more intuitive than ever before

Popular Products

Show More

Quick Help

Show More

Frequently Asked Questions

Show More

For Kotak Bank Customers

For Kotak811 Customers

Experience the all-new Kotak Netbanking Lite

Simpler, smarter & more intuitive than ever before. Now accessible on your mobile phone!

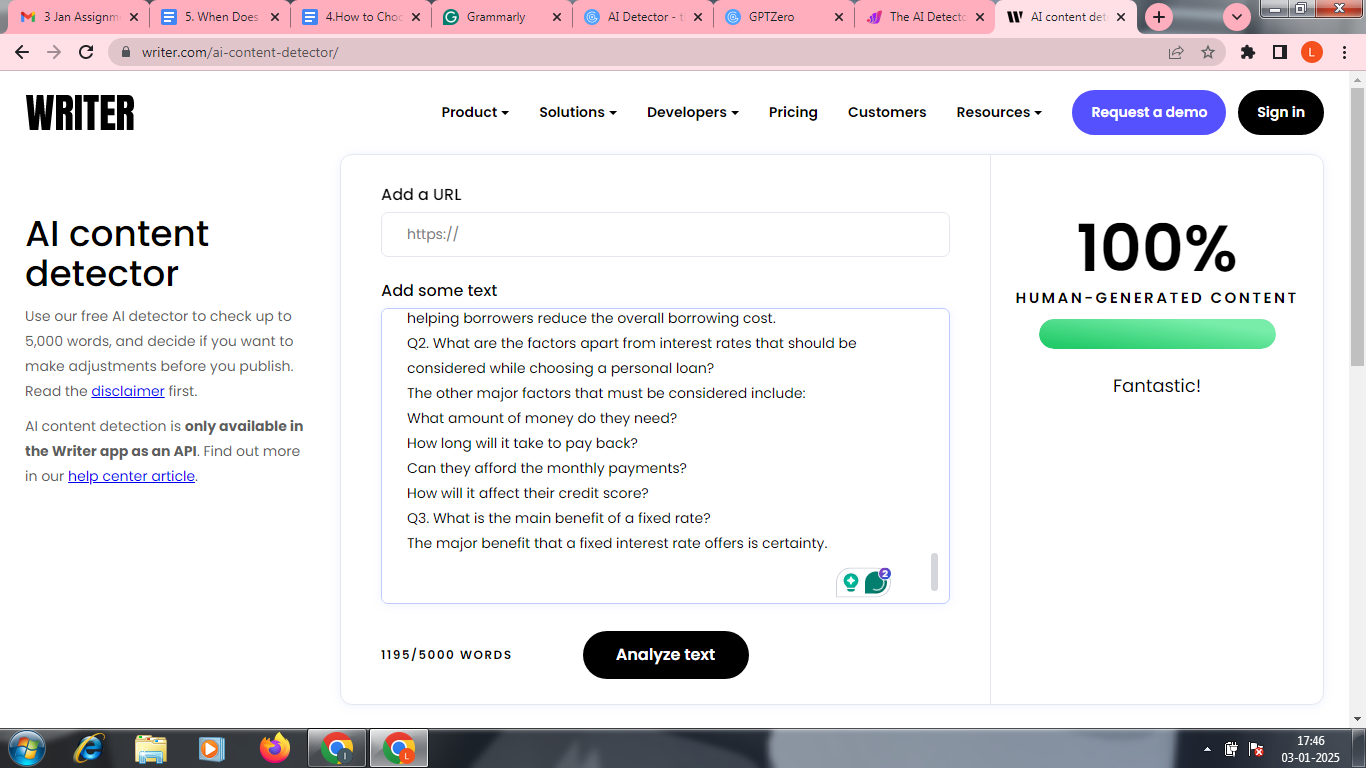

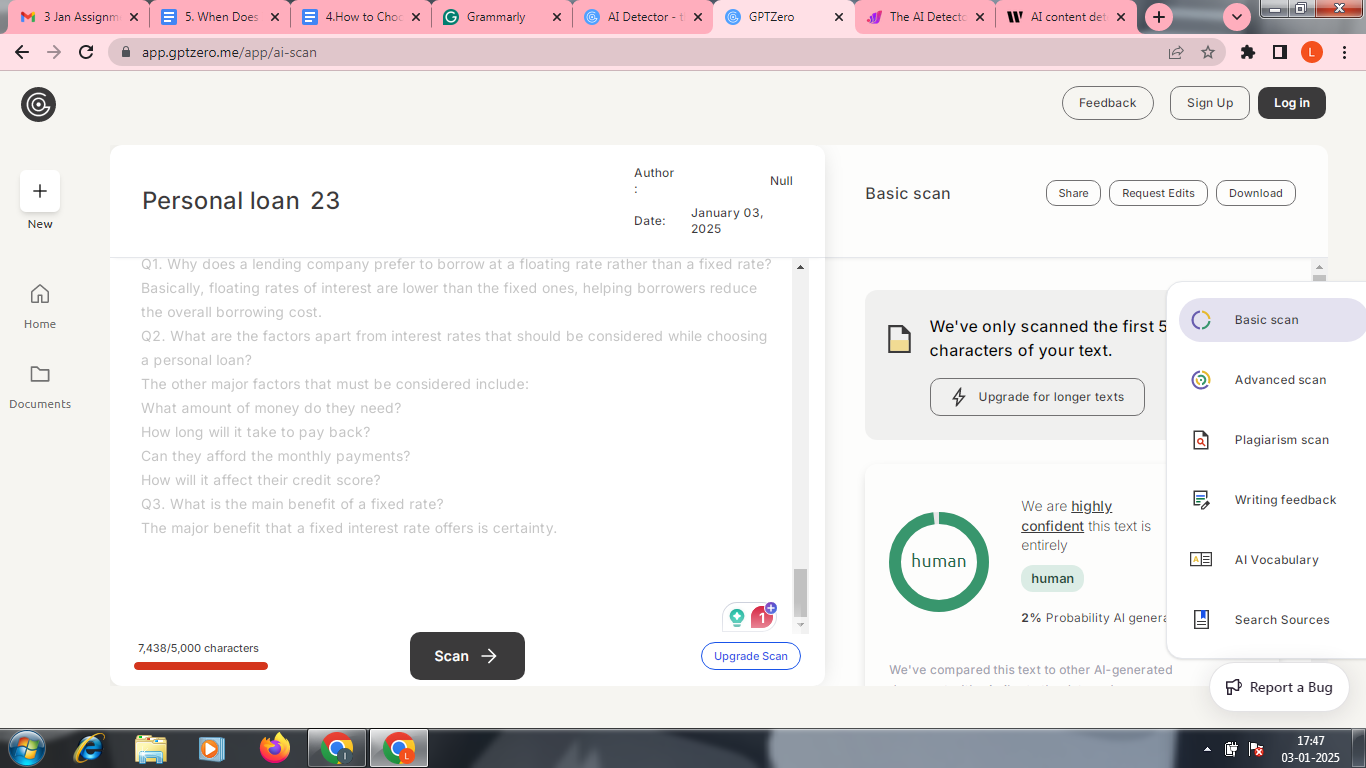

Basically, floating rates of interest are lower than the fixed ones, helping borrowers reduce the overall borrowing cost.

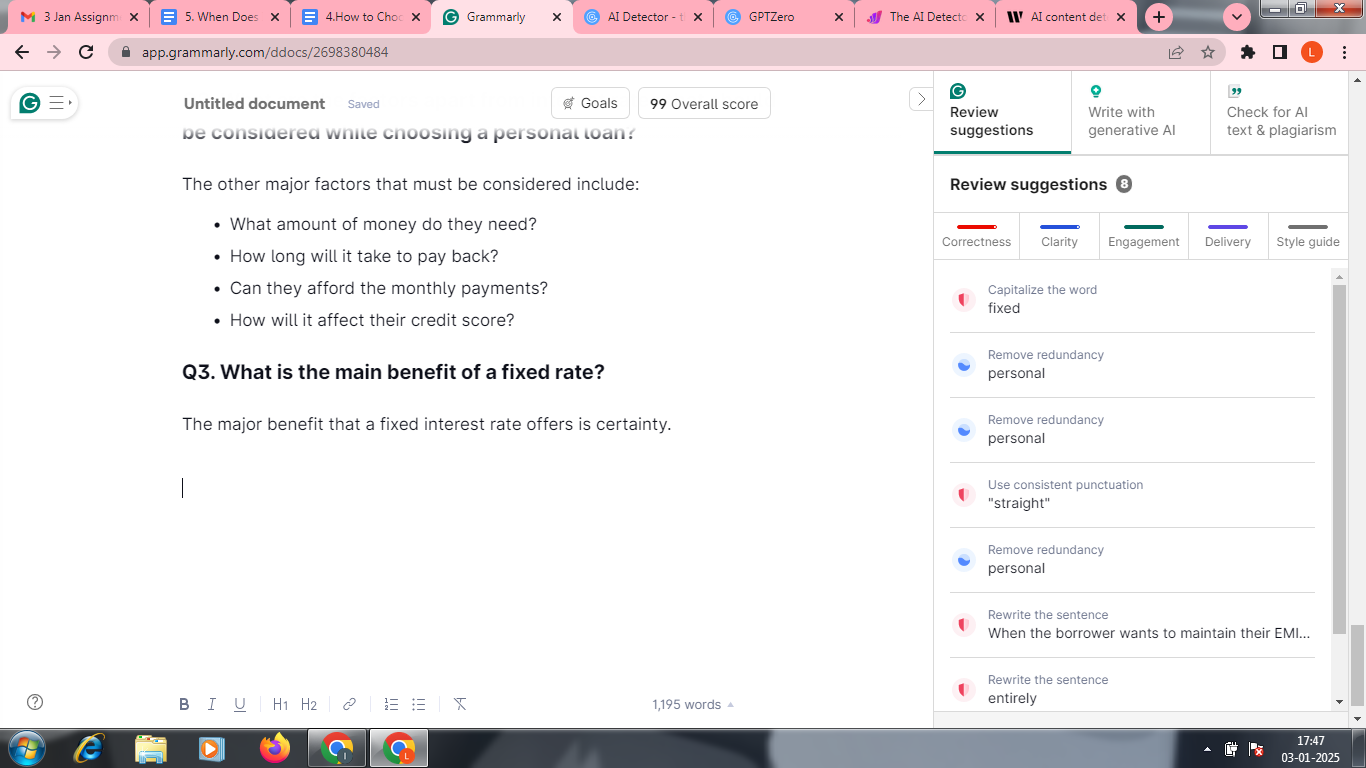

The other major factors that must be considered include:

● What amount of money do they need?

● How long will it take to pay back?

● Can they afford the monthly payments?

● How will it affect their credit score?

The major benefit that a fixed interest rate offers is certainty.

Disclaimer: This Article is for information purposes only. The views expressed in this Article do not necessarily constitute the views of Kotak Mahindra Bank Ltd. (“Bank”) or its employees. The Bank makes no warranty of any kind with respect to the completeness or accuracy of the material and articles contained in this Article. The information contained in this Article is sourced from empaneled external experts for the benefit of the customers and it does not constitute legal advice from the Bank. The Bank, its directors, employees and the contributors shall not be responsible or liable for any damage or loss resulting from or arising due to reliance on or use of any information contained herein. Tax laws are subject to amendment from time to time. The above information is for general understanding and reference. This is not legal advice or tax advice, and users are advised to consult their tax advisors before making any decision or taking any action.

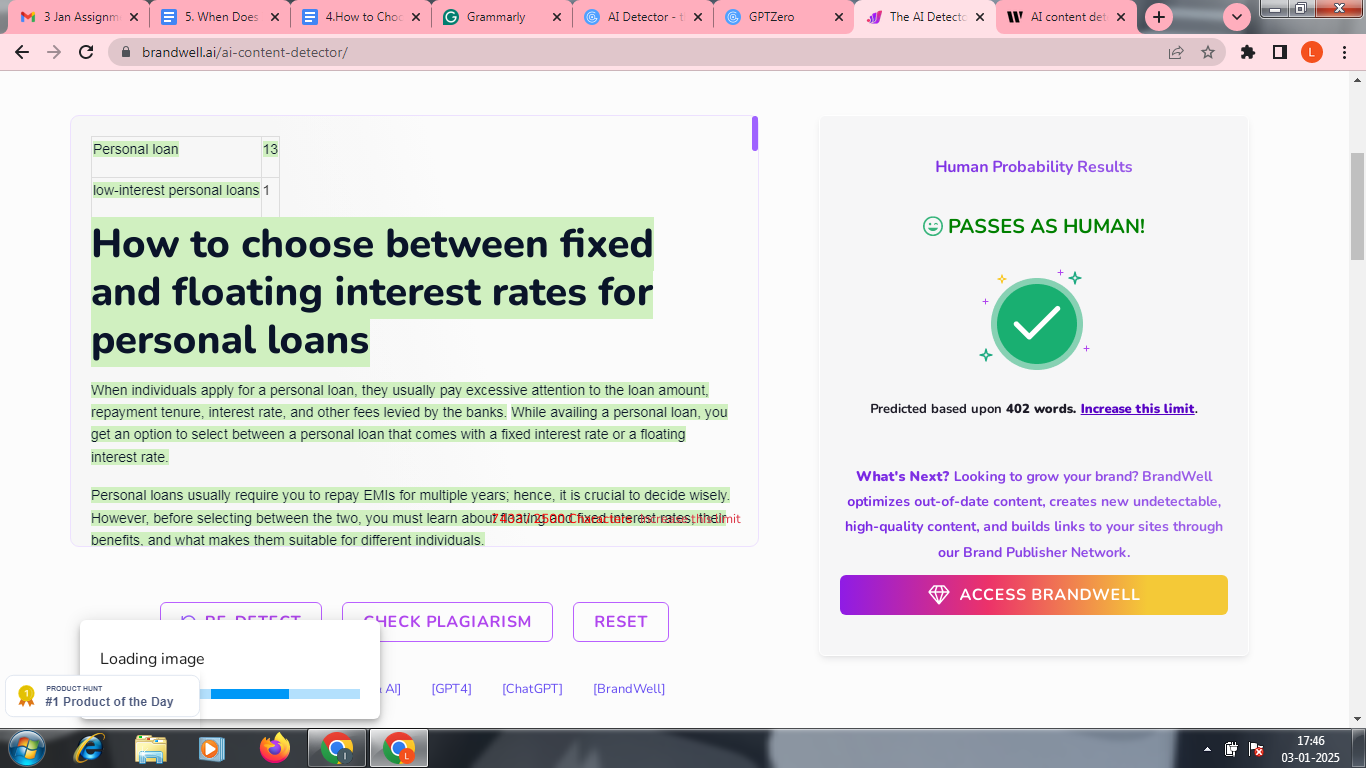

When individuals apply for a Personal Loan, they usually pay excessive attention to the loan amount, repayment tenure, interest rate, and other fees levied by the Banks. While availing a Personal Loan, you get an option to select between a Personal Loan that comes with a fixed interest rate or a floating interest rate.

Personal loans usually require you to repay EMIs for multiple years; hence, it is crucial to decide wisely. However, before selecting between the two, you must learn about floating and fixed interest rates, their benefits, and what makes them suitable for different individuals.

Understanding a Fixed Interest Rate

Under a fixed interest rate of a Personal Loan, the interest charged from individuals stays at a constant rate for the complete loan tenure. Borrowers get to check their fixed monthly income as they need to pay EMI under fixed interest rates at certain periods and, hence, plan all their finances accordingly. However, the fixed rate of interest is usually set at an increased margin of 1 – 2% against flexible rates.

Furthermore, under the fixed interest rate of Personal Loans, the first few years of repayment are utilised to cover the interest part of the loan and not the principal loan amount. Hence, a gradual shift occurs to the principal amount in the later years of the tenure.

Benefits of Fixed Interest Rates

Individuals who are willing to opt for fixed interest rates for their Personal Loans can enjoy the following benefits:

Understanding Floating Interest Rates

In Personal Loans with floating interest rates, the rate of interest stands subject to periodic revisions due to fluctuations in the repo rate, which is a benchmark established by the RBI. In floating interest rates, lenders create a margin for the rate and acknowledge the rate of interest, which is known as the Repo Linked Lending Rate or RLLR. Hence, with any fluctuations in the repo rate, there is a change in your rate of interest applicable to the Personal Loan.

Benefits of Floating Interest Rates

A Personal Loan with a floating interest rate comes with the following benefits for the borrowers:

Select Between Fixed and Floating Interest Rates: Factors to Consider

A borrower applying for a Personal Loan might be confused between selecting a floating and fixed interest rate. The key factors listed below must be considered while selecting between the two:

Fixed vs. Floating Interest Rates

It stands ideal for the borrowers to select a fixed interest rate under the following situation:

However, the floating rates of interest are suitable in the following circumstances:

Selecting a better alternative between floating and fixed interest rates depends on your financial convenience when applying for a Personal Loan.

Summing up

Most Personal Loan borrowers select a floating rate of interest over a fixed one. However, as you can see, there are benefits for both of them. Ultimately, the final decision is the borrower's. Hence, they must carefully acknowledge the benefits and other details by making an in-depth comparison online. Selecting between a fixed and a floating interest rate also depends on multiple factors, such as loan repayment period, financial situation, and risk appetite.

Kotak Mahindra Bank offers you convenience with low-interest Personal Loans followed by multiple benefits and features. For those prioritising stability, Kotak Mahindra Bank offers a fixed interest rate for peace of mind with predictable repayment.

Ready to choose the right interest rate for your needs? Apply for a Kotak Personal Loan today and explore your options!

OK